Issue Description

Based on Instruction No. 025 dated 10 October 2024, CIT is imposed on free goods and winning prizes that are the enterprise’s inventory by recognizing revenue equivalent to the Cost of Goods Sold (“COGS”) while the COGS of free goods and winning prizes is treated as a deductible expense.

Recognizing the provision of free goods and winning prizes as revenue effectively means that these expenses will not be allowed as deductible for CIT purposes. From a commercial perspective, there is no actual revenue generated from providing free goods and winning prizes. This deemed revenue approach will significantly increase the effective tax rate for companies that utilize free goods and winning prizes as part of their promotional schemes, diverging from international practices, including the International Financial Reporting Standards (IFRS) and tax practices in ASEAN.

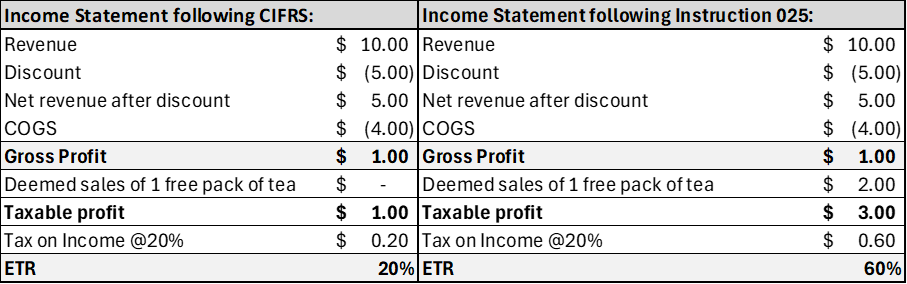

Example of the increase in Effective Tax Rate (ETR) due to deemed revenue clause in Instruction 025:

Promotion scheme: 1 buy pack of tea, get 1 pack of tea for free. The selling price of 1 pack of tea is US$ 5. Cost of goods sold (COGS) is US$2. Impact on ETR is as follows:

Impact on business

Potential impacts on businesses if the provision of free goods and winning prizes from the company’s inventory is deemed as revenue :

- Business downsizing due to sales’ decline;

- Huge increase in effective tax rate which is one of the factors determining investment decisions;

Recommendation

- Remove the imposition of CIT on deemed revenue arising from Promotional Goods.

In line with international best practices and regional tax standards, we respectfully recommend that the GDT review the current tax treatment of Promotional Goods. Specifically, free goods and winning prizes provided from an enterprise’s inventory for promotional purposes should not be treated as taxable revenue, but rather recognized as deductible business expenses for CIT purposes.

Royal government of Cambodia

Initiative from Eurocham: The issue has been raised by the Tax & Governance Committee within The White Book edition 2027 in the Recommendation No. 60.

National Counterparts

General Department of Taxation